College education is becoming more expensive every year. Tuition fees, hostel charges, books, travel, and other expenses can be a big burden for most families. An education loan is a smart way to manage these costs without using all your savings.

In this blog, you will learn in simple and clear language:

- What is an education loan

- Which expenses can be covered

- Step-by-step process: how to pay college fees through education loan

- How the bank sends money to the college

- When and how you have to repay

- EMI calculation with an easy example

- Useful tips to reduce interest and repay comfortably

This guide is helpful for students and parents planning higher studies in India or abroad.

What Is an Education Loan?

An education loan is money given by a bank or financial institution to help you pay for education-related expenses. You do not have to pay back the full amount immediately. You get time to study, complete the course, and then start repaying in monthly instalments.

What expenses does an education loan cover?

Most banks allow the loan to be used for:

- Tuition fees

- Hostel and mess charges

- Exam, lab, and library fees

- Books, laptop, uniforms, and equipment

- Travel expenses (for study abroad)

- Insurance premium for student (in case of study abroad)

This means you can use the loan not just for college fees, but for almost all major study-related costs.

Key Terms You Must Understand

Before taking an education loan to pay college fees, learn these simple terms:

- Principal: The loan amount you borrow.

- Example: If you take a loan of ₹8,00,000, then ₹8,00,000 is your principal.

- Example: If you take a loan of ₹8,00,000, then ₹8,00,000 is your principal.

- Interest Rate: Extra percentage charged by the bank on the principal.

- Example: If the interest rate is 10% per year, you pay 10% of the remaining loan amount as interest every year.

- Example: If the interest rate is 10% per year, you pay 10% of the remaining loan amount as interest every year.

- Moratorium Period: Time during which you don’t have to pay full EMIs. Usually this is course period + 6 months or 12 months after getting a job (varies by bank). During this period, interest keeps adding.

- EMI (Equated Monthly Instalment): Fixed amount you pay every month after the moratorium period to repay the loan.

- Tenure: Total time given by the bank to repay the loan, usually 5 to 15 years.

- Collateral: Security given to the bank like property, fixed deposit, etc., for higher loan amounts.

Knowing these terms makes it easier to compare loans and understand your responsibility.

Step-by-Step Process to Pay College Fees Through Education Loan

Let’s see how you actually use an education loan to pay your college fees.

Step 1: Get Admission or Conditional Offer

First, you must apply to colleges and get an admission letter or at least a conditional offer. Banks usually ask for:

- Admission letter

- Fee structure or fee schedule

- Course details and duration

Without proof of admission or offer, most banks will not process the education loan.

Step 2: Check Eligibility for Education Loan

Every bank has basic rules. Common conditions are:

- Student must be an Indian citizen (for Indian banks)

- Confirmed admission in a recognised institution

- Course must be job-oriented (professional, technical, or degree courses)

- Parent/guardian is usually taken as co-borrower

Some banks may also consider your academic record and entrance exam scores.

Step 3: Decide Loan Amount

Now calculate how much money you actually need.

Example: Total Cost Calculation

Suppose you are joining a 4-year B.Tech course.

- Tuition fees: ₹1,50,000 per year × 4 = ₹6,00,000

- Hostel + mess: ₹80,000 per year × 4 = ₹3,20,000

- Books and other expenses: ₹20,000 per year × 4 = ₹80,000

Total estimated cost = ₹6,00,000 + ₹3,20,000 + ₹80,000 = ₹10,00,000

Maybe your parents can pay part of it from their savings. Suppose they can pay ₹2,00,000.

So, education loan required = ₹10,00,000 – ₹2,00,000 = ₹8,00,000

This is the amount you can ask from the bank.

Step 4: Compare Education Loan Options

Do not take the first loan you see. Compare:

- Interest rate (fixed or floating)

- Processing fees

- Moratorium period (course period + 6 or 12 months)

- Maximum repayment tenure

- Prepayment charges (if you want to close early)

- Margin money (some banks will ask parents to pay a small percentage of cost)

Choose a bank that offers:

- Lower interest rate

- Flexible repayment

- Minimal fees

Step 5: Apply for the Education Loan

You can apply:

- Online through the bank’s portal, or

- By visiting the nearest bank branch

Common documents required:

- Student’s KYC (ID proof, address proof, photos)

- Parent/guardian KYC

- Income proof of co-borrower (salary slips, ITR, bank statements)

- Admission letter and fee structure

- Academic records (mark sheets, certificates)

- Collateral documents (if applying for a high amount)

Fill the form carefully and submit all documents. The bank will verify your details and may ask some questions.

Step 6: Loan Sanction Letter

If the bank approves, it will issue a sanction letter. This letter clearly shows:

- Sanctioned loan amount

- Interest rate

- Tenure

- Moratorium details

- Repayment terms

Keep this letter safe. Some colleges may ask for it as proof of funds.

How Does the Bank Pay the College Fees?

This is a very important part. Many students think the bank will give all the money to them in cash. That is not correct.

Most banks follow these steps:

- The college gives a fee schedule (for example, semester-wise or year-wise).

- The bank approves the total loan amount based on this schedule.

- At the time of fee payment, the bank directly transfers the tuition fees to the college’s bank account using NEFT/RTGS or a demand draft.

- For hostel and other approved expenses, the bank may:

- Either send the money to the college, or

- Credit the amount to the student’s or parent’s bank account on proof of expense (like hostel bill, laptop bill, etc.).

- Either send the money to the college, or

Example of Fee Disbursal

Suppose your 1st year tuition fee is ₹1,50,000 and hostel charges are ₹80,000.

- At the start of the year, college gives you a fee demand letter.

- You submit this letter to the bank.

- The bank transfers ₹1,50,000 directly to the college.

- Hostel amount of ₹80,000 is either paid to the college or given to you (as per bank policy).

This process repeats every semester or every year until your course is complete, within the approved loan amount.

When Do You Start Repaying Your Education Loan?

Repayment usually does not start immediately after disbursal.

Most banks allow:

- Moratorium = Course duration + 6 months or 12 months (varies by bank).

During this period:

- You generally don’t pay full EMIs.

- But interest keeps adding to your loan amount.

- Some banks ask you to pay only simple interest or partial interest during this time.

Starting to pay at least the interest during the moratorium is a good habit because it reduces the total cost.

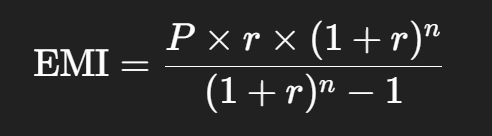

EMI Calculation Example (Very Simple)

Let’s take a practical example so you can understand how much you may have to pay every month.

Example Details

- Loan amount (Principal): ₹8,00,000

- Interest rate: 10% per annum

- Repayment tenure: 10 years (120 months)

We will use the standard EMI formula:

Where:

- P = Principal (₹8,00,000)

- r = Monthly interest rate = 10% / 12 = 0.10 / 12 ≈ 0.00833

- n = Number of months = 10 × 12 = 120

Without going into complex calculation steps, the approximate EMI comes to around ₹10,600–₹10,800 per month (rounded value; exact EMI depends on bank calculation).

Let’s take ₹10,700 per month as an approximate EMI.

What does this mean?

- You borrowed ₹8,00,000.

- You will pay about ₹10,700 every month for 10 years.

- Total amount paid ≈ ₹10,700 × 120 = ₹12,84,000

So, roughly ₹4,84,000 is the interest paid over 10 years on an ₹8,00,000 loan at 10% interest.

This example shows why you should:

- Try to reduce interest rate by choosing the right bank.

- Avoid borrowing more than you really need.

- Start prepayments whenever your income increases.

Tips to Pay College Fees Smartly Through Education Loan

Here are some useful tips to manage your education loan wisely:

Borrow Only What You Need

Calculate total cost carefully and avoid taking a much higher amount “just in case”. Higher loan means:

- Higher EMIs

- More total interest

Start Paying Interest During the Course

If your family can afford, pay at least the interest during the moratorium period. This will:

- Reduce the final outstanding amount

- Lower total interest paid

- Reduce your future EMI burden

Choose a Longer Tenure but Prepay When Possible

A longer tenure gives a smaller EMI, which is easier to manage when your starting salary is low. Later, when your income increases, you can:

- Prepay part of the loan, or

- Increase EMI amount

This reduces total interest.

Use Scholarships and Part-Time Work

If you win any scholarship or do a part-time job:

- Use that money to pay some part of your fees or to prepay your loan.

- This can significantly reduce your overall loan burden.

Keep All Fee Receipts and Documents

Always keep:

- Fee receipts

- Hostel bills

- Book purchase bills

- Insurance and travel receipts

Banks may ask for these documents before disbursing the amount, especially for non-tuition expenses.

Common Mistakes to Avoid

When paying college fees through an education loan, avoid these mistakes:

- Not reading loan terms carefully

- Many students only look at the interest rate and ignore other charges and conditions.

- Many students only look at the interest rate and ignore other charges and conditions.

- Missing payments after moratorium

- Late or missed EMI payments can hurt your (or your parent’s) credit score.

- Late or missed EMI payments can hurt your (or your parent’s) credit score.

- Using loan money for non-education expenses

- This increases your debt without helping your career.

- This increases your debt without helping your career.

- Not updating the bank about changes

- If your course duration changes, or you switch college, inform the bank in time.

Simple Summary of the Process

Let’s quickly recap the steps:

- Get admission or offer from a recognised college.

- Calculate total education cost and decide how much loan you need.

- Compare education loans from different banks (interest, tenure, fees).

- Apply for the loan with all required documents.

- Receive sanction letter from the bank.

- Submit college fee schedule and demand letter to the bank.

- Bank transfers tuition fees directly to the college and releases other approved amounts as per rules.

- You complete your course, get a job, and start paying EMIs after the moratorium period.

- You can prepay the loan early to save on interest.

Final Thoughts

Paying college fees through an education loan is a safe and structured way to fund your education if you plan carefully. It allows you to study in a good college today and repay later when you start earning.

The key points to remember are:

- Understand the loan terms clearly.

- Borrow only what you genuinely need.

- Track how the bank is paying your fees to the college.

- Start repaying responsibly as soon as you can.

If used wisely, an education loan is not a burden – it is a stepping stone that helps you build your career and future income, while protecting your family’s savings today.