Pursuing higher education is a dream for many, but the costs involved often make students and parents consider education loans. While applying for a loan, one term that comes up frequently is the CIBIL score. This three-digit number can determine whether your loan gets approved, the interest rate you receive, and even the maximum amount you can borrow. In this guide, we will explain everything about checking your CIBIL score, its importance for education loans, and practical steps for how to check the CIBIL score for an education loan.

What is a CIBIL Score?

A CIBIL score is a number between 300 and 900 that represents your creditworthiness. It is maintained by TransUnion CIBIL, a credit information company in India. This score reflects your financial behavior and history in repaying loans and using credit cards.

How the Score is Calculated

- Payment History (35%) – Timely repayment of loans and credit card bills.

- Credit Utilization (30%) – Ratio of credit used vs. total credit available.

- Credit Age & Mix (15%) – Longer credit history and variety of credit improves score.

- Hard Inquiries (10%) – Multiple loan or credit card applications in a short period lower the score.

- Other Factors (10%) – Such as defaults, settled loans, or overdue payments.

Understanding Score Ranges

| CIBIL Score | Creditworthiness | Loan Approval Impact |

| 750-900 | Excellent | Easy approval, better interest rates |

| 700-749 | Good | Approval likely, moderate interest rates |

| 650-699 | Fair | Approval may require co-applicant |

| <650 | Poor | Difficult approval, higher interest |

Example:

If Riya has a CIBIL score of 780, she is likely to get her education loan approved with a lower interest rate. But if her score is 620, she may either get rejected or require her parent as a co-applicant with a better credit score.

Why CIBIL Score is Important for Education Loans

1. Loan Approval

Banks use your CIBIL score to assess the risk of lending. A high score signals reliability, while a low score indicates potential default. Most lenders prefer a score of 700 or above for education loans.

2. Better Loan Terms

A good CIBIL score can help you secure:

- Lower Interest Rates: Reduces the overall repayment amount.

- Higher Loan Amounts: Covers more of tuition fees and other expenses.

- Faster Approval: Loan applications are processed quickly.

Example Calculation:

Suppose a student applies for a loan of ₹12 lakh for 5 years:

| CIBIL Score | Interest Rate | EMI (Monthly) | Total Payment |

| 780 | 9% | ₹24,730 | ₹14,83,800 |

| 700 | 11% | ₹26,680 | ₹16,00,800 |

| 650 | 13% | ₹28,690 | ₹17,21,400 |

Observation: A higher CIBIL score can save ₹1.5 lakh to ₹2 lakh over 5 years.

3. Role of Co-Applicant

If a student does not have a credit history, the co-applicant (usually a parent) plays a crucial role. Lenders look at the co-applicant’s CIBIL score to decide loan approval.

How to Check the CIBIL Score for an Education Loan?

Checking your CIBIL score is simple and can be done in multiple ways:

1. Through the Official CIBIL Website

- Visit CIBIL’s official portal.

- Provide your PAN, date of birth, and contact details.

- You can get one free report per year.

- Useful for understanding your current credit status before applying for a loan.

2. Mobile Applications

Apps like Paytm, PhonePe, and Google Pay allow users to check their CIBIL score instantly. This is convenient for students who prefer digital solutions.

3. Third-Party Financial Platforms

Some banks and fintech platforms, including ICICI Bank, MoneyView, and Bajaj Finserv, offer free CIBIL score checks. They may also provide personalized recommendations to improve your score.

Tip: Always ensure you use reliable and official sources to check your score to avoid fraud or inaccurate reports.

Steps to Improve Your CIBIL Score

If your score is below the desired threshold, improving it before applying for a loan can save you money and stress.

1. Pay Bills on Time

Late payments are one of the biggest factors that reduce your score. Ensure all loans and credit card bills are paid by the due date.

2. Maintain Low Credit Utilization

Use less than 30% of your total credit limit.

Example:

If your credit card limit is ₹50,000, keep your spending below ₹15,000 to maintain a healthy score.

3. Avoid Multiple Loan Applications

Applying for multiple loans or credit cards within a short period can create too many hard inquiries, reducing your score.

4. Monitor Your Credit Report

Check your report regularly for errors or discrepancies. If you find inaccuracies, raise disputes with CIBIL immediately.

CIBIL Score and Government Schemes

Some schemes relax the CIBIL score requirement for students:

Pradhan Mantri Vidya Lakshmi Yojana (PM-Vidya Lakshmi)

- Students can avail loans up to ₹10 lakh without a CIBIL score.

- This scheme targets students who don’t have a credit history but require financial support for higher education.

Example:

If a student hasn’t had a previous loan or credit card, they can still get a loan of ₹8 lakh under this scheme without worrying about their CIBIL score.

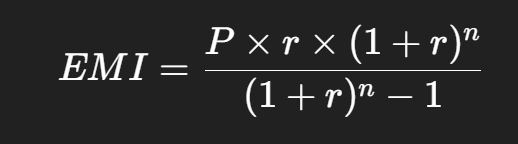

Calculating EMIs for Education Loans

Understanding EMI calculations can help students plan repayments better. The formula for EMI calculation is:

Where:

- P = Loan principal

- r = Monthly interest rate (annual rate / 12 / 100)

- n = Loan tenure in months

Example Calculation:

Loan: ₹10 lakh, Interest Rate: 10%, Tenure: 5 years (60 months)

Total Payment: ₹21,250 × 60 = ₹12,75,000

This shows how a lower interest rate due to a higher CIBIL score can save a student a significant amount.

Final Thoughts

Checking and maintaining your CIBIL score is crucial before applying for an education loan. A high score ensures:

- Easier loan approval

- Lower interest rates

- Higher loan amounts

- Better repayment terms

Start by checking your score today and take steps to improve it if needed. Even small actions like timely payments or reducing credit utilization can make a big difference.

Remember: Your financial discipline today will directly impact your education and career opportunities tomorrow.