Higher education is expensive. Many students want to do a master’s degree or other graduate course, but they worry about fees, living costs, and other expenses. A graduate study loan can help you manage money so you can focus on your studies.

In this blog, we will understand:

- What is a graduate study loan?

- Types of graduate study loans

- Important terms like interest rate, tenure, EMI

- How to compare and choose the best loan

- Step-by-step process to apply

- Example with calculations

- Tips to reduce loan burden

- Common mistakes to avoid

The language is very simple, so even first-time borrowers can understand clearly.

What Is a Graduate Study Loan?

A graduate study loan is money that a bank or financial institution gives you to pay for your postgraduate or graduate-level education. You have to repay this money later with interest.

You can use a graduate study loan to pay for:

- Tuition fees

- Exam and registration fees

- Books and study material

- Hostel or rent

- Food and living expenses

- Laptop or equipment (if allowed by lender)

You usually don’t need to repay the loan immediately. Many lenders allow you to start repayment after your course ends or after a grace period.

Types of Graduate Study Loans

Graduate study loans can be divided into a few main types. Knowing these helps you choose the right one.

Government or Federal Graduate Loans (Country-Specific)

In some countries (like the US), there are federal or government-backed loans for graduate students. These loans often have:

- Fixed interest rates

- More protection for borrowers

- Options like income-based repayment, deferment, etc.

However, there may be limits on how much you can borrow.

(If you are not in such a system, you will mainly use bank or private loans.)

Private Graduate Study Loans

Private loans are given by banks, credit unions, or private financial companies. These loans:

- Can cover high tuition and living costs

- May have fixed or variable interest rates

- Often require good credit score or a co-signer/guarantor

They can be more flexible in loan amount, but sometimes more expensive if interest is high.

Secured vs Unsecured Graduate Loans

Some lenders ask for security or collateral (like property, fixed deposit). These are secured loans.

- Secured loan

- Requires collateral

- Usually lower interest rate

- Suitable for large loan amounts

- Unsecured loan

- No collateral needed

- Higher interest rate

- Based on your or your co-signer’s income and credit score

Key Terms You Must Understand

Before taking a graduate study loan, you must know some basic financial terms.

Principal

The principal is the amount of money you borrow.

If you borrow $20,000 for your graduate program,

Principal = $20,000

Interest Rate

Interest rate is the extra percentage you pay on the principal every year.

- It can be fixed (same rate for full tenure)

- Or variable (changes with market conditions)

Example: If your interest rate is 8% per year, and you borrow $10,000, then in one year the interest is around $800 (simple example).

Tenure (Loan Term)

Tenure is the time you get to repay the loan, usually in years.

- Graduate loans may have tenure of 5, 10, 15 or even 20 years

Longer tenure = smaller monthly EMI, but more total interest paid.

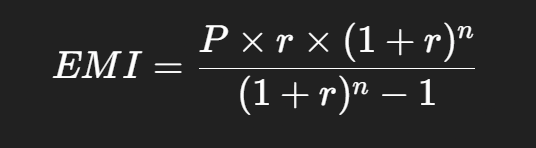

EMI (Equated Monthly Instalment)

EMI is the fixed amount you pay every month to repay loan plus interest.

EMI depends on:

- Principal (loan amount)

- Interest rate

- Tenure

We will do detailed EMI calculation example later.

What Can a Graduate Study Loan Cover?

Most graduate loans can be used for:

- Tuition fees charged by the college/university

- Examination, library, lab, and other academic fees

- Books, study materials, laptop (if included in loan scheme)

- Living expenses (hostel, rent, food, transport)

- Health insurance (for international students, if allowed)

Always check with the lender exactly what expenses are covered.

Eligibility for a Graduate Study Loan

Requirements may vary, but usually include:

- You must have completed your undergraduate degree

- You must have an admission offer from a recognized university or college

- Good academic record improves chances

- A co-signer/guarantor may be needed (parent, relative, or working professional)

- In private loans, a good credit score helps you get lower interest rate

Some lenders also check:

- Course type (full-time, part-time, online)

- College ranking or recognition

- Job prospects after course

How to Compare Graduate Study Loans

There may be many lenders offering loans for graduate study. Do not choose only based on the first offer. Compare these points:

Interest Rate

- Check if the rate is fixed or variable

- Even a difference of 1–2% makes a big change in total cost over many years

Processing Fee and Other Charges

Some lenders take:

- Processing fee (a small percentage of loan amount)

- Late payment charges

- Prepayment or foreclosure charges

Always ask for a full list of fees.

Repayment Flexibility

Check:

- When does repayment start? (after course or immediately?)

- Is there a grace period after graduation?

- Are you allowed to make extra payments without penalty?

- Are there options to postpone payments in case of financial difficulty?

Loan Amount and Coverage

- Does the loan cover 100% of tuition?

- Does it cover living expenses?

- Is there a maximum limit per year or total?

Co-signer and Collateral Requirements

- Do you need a co-signer?

- Is collateral required for the loan amount you want?

If you and your family do not have collateral, you may prefer an unsecured loan, but compare interest carefully.

Step-by-Step Process to Get a Graduate Study Loan

Here is a simple step-by-step guide:

Step 1: Research Courses and Universities

Decide:

- Which course you want

- Which country/city

- Approximate tuition fees and living costs

This helps you estimate how much loan you need.

Step 2: Check Loan Options

- Visit websites of banks and private lenders

- Use comparison sites or consult your university financial aid office

- Shortlist 3–5 lenders with good terms

Step 3: Calculate Total Cost and EMI

Use online EMI calculators or do rough calculations yourself (we’ll see an example next).

Compare total amount payable, not just interest rate.

Step 4: Prepare Documents

Common documents:

- Admission letter

- Previous academic mark sheets

- ID proof, address proof

- Income proof of you or co-signer

- Bank statements

- Collateral papers (if required)

Step 5: Apply and Get Approval

- Fill application form (online or offline)

- Attach all documents

- Answer any questions from the lender

After reviewing, the lender will approve or reject the loan. If approved, they issue a sanction letter.

Step 6: Disbursement of Loan

- Fee may be sent directly to the university

- Some part may be sent to your bank account for living expenses

Details depend on lender policy.

Example with EMI and Interest Calculations

Let’s take a simple example to understand how much you may pay.

Example:

You take a graduate study loan of $30,000

Interest rate = 8% per year (fixed)

Tenure = 10 years (120 months)

We’ll calculate a rough EMI using a standard EMI formula:

Where:

- P = Principal (loan amount)

- r = Monthly interest rate = Annual rate / 12

- n = Number of months (tenure)

Step 1: Convert Annual Interest to Monthly

Annual rate = 8% = 0.08

Monthly rate r=0.08/12≈0.006667

Step 2: Plug Values

- P=30,000

- r≈0.006667

- n=10×12=120 months

Using the formula (we’ll use an approximate result):

EMI≈$364 per month (approx)

So you pay about $364 every month for 10 years.

Step 3: Find Total Amount Payable

Total amount paid over 10 years:

EMI×n=364×120=43,680

So:

- Total paid = $43,680

- Principal = $30,000

- Total interest paid = $43,680 − $30,000

= $13,680

This shows:

- You borrowed $30,000

- You are paying back $43,680

- The extra $13,680 is the cost of borrowing (interest)

Compare with Longer Tenure Example

Now, suppose you choose a 15-year tenure instead of 10 years, same interest rate and principal.

- Loan amount = $30,000

- Interest rate = 8% per year

- Tenure = 15 years (180 months)

Approximate EMI reduces to around $287 per month.

Now total payable:

287×180=51,660

- Total paid ≈ $51,660

- Principal = $30,000

- Interest ≈ $21,660

So you pay lower EMI each month, but much higher total interest ($21,660 vs $13,680).

Conclusion from the example:

- Shorter tenure = higher EMI but less total interest

- Longer tenure = lower EMI but more total interest

You must balance monthly affordability and total cost.

Tips to Reduce Your Graduate Loan Burden

Here are some practical tips to make your graduate study loan easier to manage.

Borrow Only What You Really Need

Do not borrow extra money just because you are eligible for a higher amount. Calculate:

- Tuition fees

- Essential living costs

- Some buffer for emergencies

Try to cover part of your expenses through:

- Scholarships

- Part-time work (if allowed)

- Savings

Look for Scholarships and Grants First

Scholarships and grants are free money (no need to repay). Even a small scholarship can reduce your loan amount and interest in the long term.

Start Paying Interest Early (If Possible)

If your lender allows it, try to pay interest during your study period or pay small amounts towards principal. This reduces:

- Total interest accumulation

- Your EMI after graduation

Even paying $50–$100 per month during study years can save thousands later.

Avoid Unnecessary Expenses

While studying, try to control:

- Luxury spending

- Frequent eating out

- Unnecessary gadgets or travel

Remember: every dollar you save now can reduce how much you need to borrow.

Consider Extra Payments After Graduation

When you start working, if your income allows, try to:

- Pay more than your EMI sometimes

- Use bonuses or extra income to prepay part of the loan

This can reduce tenure and interest significantly. But first, check if the lender has prepayment charges.

Common Mistakes Students Make

Try to avoid these mistakes when taking a graduate study loan.

Ignoring Total Cost

Many students only look at the monthly EMI and choose the lowest one, but forget that:

- Lower EMI often means longer tenure

- Longer tenure means much more total interest

Always check total repayment amount.

Not Reading Terms and Conditions

Never sign loan documents without reading:

- Interest rate details

- Extra charges (late fee, processing fee, prepayment fee)

- When repayment starts

- What happens if you miss payments

Delaying Payments Without Reason

Some students delay repayment even when they have income, just to keep more cash in hand. This increases interest and can hurt credit score if payments are late.

Not Using a Co-signer with Better Credit

If your own credit score or income is low, adding a co-signer with strong credit can:

- Help you get approval easier

- Sometimes get lower interest

Not using this option can cost you more.

Taking Variable Rate Without Understanding Risk

A variable interest rate may start low, but it can increase later. If you are not comfortable with risk, you may prefer a fixed rate for stability.

How to Make Your Graduate Study Loan Work for You

A loan is not always a burden. It can be a smart investment if:

- You choose a course with good job prospects

- You study seriously and build skills

- You manage your money wisely

Think of your graduate study loan as a tool to open doors to:

- Better salary

- Better career growth

- More knowledge and experience

But like any tool, it must be used carefully.

Simple Checklist Before You Apply

Use this checklist to stay confident and organized:

- Course and college decided?

- Total cost of study calculated? (tuition + living + other fees)

- Scholarships or grants researched?

- Loan options compared? (3–5 lenders)

- Interest rate, fees, and tenure compared?

- EMI calculated for different tenures?

- Co-signer/guarantor ready? (if needed)

- All documents prepared?

- Terms and conditions read and understood?

- Repayment plan after graduation roughly planned?

If you can say “yes” to most of these, you are ready to apply with confidence.

Final Thoughts

A graduate study loan can feel scary at first because it is a big financial decision. But with proper information and planning, it becomes manageable and even helpful.

Remember these key points:

- Understand interest, tenure, EMI, and total cost

- Compare different lenders carefully

- Borrow only what you need

- Try to pay interest early or make extra payments when possible

- Avoid common mistakes like ignoring terms or choosing only based on lowest EMI

With the right approach, your graduate study loan can support your dream of higher education and a better career, instead of becoming a burden. Use this guide as your starting point, and take each step calmly and carefully.