Pursuing an MBBS in a private college is often a dream for many students. However, the high tuition fees, hostel charges, and other educational expenses make it difficult for families to fund medical education entirely from savings. This is where education loans play a critical role. Education loans help students access high-quality private medical education without financial stress, allowing them to focus on their studies and future career.

This comprehensive guide explains everything you need to know about an education loan for mbbs in private college, including loan amounts, interest rates, repayment options, eligibility criteria, collateral requirements, examples, calculations, and tips. By the end, you’ll understand how to plan your MBBS loan efficiently and manage repayments after your medical education.

Why Education Loans Are Important for MBBS Students

Medical education is expensive in India, especially in private colleges. While government medical colleges have lower tuition fees (usually ₹5–15 lakh for the full course), private colleges can charge ₹20 lakh to ₹50 lakh or more for the entire MBBS program. These costs often include:

- Tuition fees

- Hostel or accommodation fees

- Library and laboratory charges

- Exam fees and other miscellaneous expenses

Education loans allow students to cover these costs upfront while repaying the loan gradually after completing their course. The benefits include:

- Access to quality private education without upfront payment

- Flexible repayment options with moratorium periods

- Tax benefits under Section 80E of the Income Tax Act

- Loans based on future earning potential rather than current financial status

Education Loan for MBBS in Private Colleges

The loan amount depends on whether the loan is secured (requires collateral) or unsecured (no collateral required). Banks and NBFCs usually offer:

- Unsecured Loans: Up to ₹30 lakh

- Secured Loans: Up to ₹50 lakh or more

Example Scenario

| Expense Type | Cost (₹) |

| Tuition Fee | 30,00,000 |

| Hostel Fee | 3,00,000 |

| Books & Supplies | 1,00,000 |

| Miscellaneous | 1,00,000 |

| Total | 35,00,000 |

- Using an unsecured loan: ₹30 lakh (remaining ₹5 lakh must be arranged separately or with collateral)

- Using a secured loan: Full ₹35 lakh can be covered with collateral

Platforms like Propelld and GyanDhan help students calculate how much they can borrow based on the co-applicant’s income and credit profile.

Interest Rates

Interest rates vary by lender and loan type. Typically:

- Unsecured loan: 8.55% – 10% per annum

- Secured loan: 9% – 12% per annum

Lower interest rates are often available for students with strong co-applicants (parents with high income and good credit history) or loans backed by government schemes.

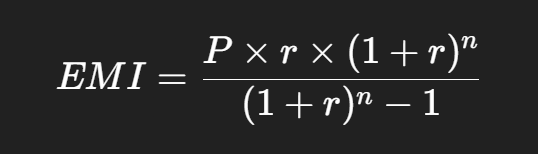

EMI Calculation Example

Suppose a student borrows ₹30 lakh at 9% per annum for 10 years after a moratorium period.

EMI formula:

Where:

- P = Principal = ₹30,00,000

- r = Monthly interest rate = 9% ÷ 12 = 0.0075

- n = Total months = 10 × 12 = 120

EMI ≈ ₹38,100 per month

This amount can vary depending on interest compounding, loan tenure, and moratorium period.

Repayment Terms

Education loans for MBBS come with flexible repayment options to ensure students can repay comfortably after starting their careers.

- Course Duration: 5.5 years including internship

- Moratorium Period: Course duration + 12 months

- Repayment Tenure: 12 to 15 years

Example

If a student borrows ₹30 lakh, the repayment schedule could look like:

| Year | Principal Outstanding (₹) | EMI (₹) |

| 1–6 (Moratorium) | 30,00,000 | Interest may be paid or capitalized |

| 7 | 30,00,000 | 38,100 |

| 7–16 | Decreasing principal | 38,100/month |

Most lenders allow partial interest payments during the moratorium, which reduces the total interest paid over the tenure.

Collateral Requirements

Whether you need collateral depends on the loan amount:

- Unsecured Loan: No collateral required (up to ₹30 lakh)

- Secured Loan: Property, fixed deposit, or other assets as collateral (for amounts above ₹30 lakh)

Example: For a ₹45 lakh MBBS course, ₹30 lakh may be covered without collateral, while the remaining ₹15 lakh requires property or other security.

Eligibility Criteria

Eligibility varies slightly across banks and NBFCs, but general criteria include:

- Student Eligibility:

- Must have cleared NEET or other recognized entrance exams

- Admission must be in a recognized medical college

- Must have cleared NEET or other recognized entrance exams

- Co-applicant:

- Parent or guardian with stable income

- Good credit score

- Age 35–60 years (for most banks)

- Parent or guardian with stable income

- Loan Amount Criteria:

- Amount required, collateral availability, and lender policies

- Age of Student:

- 18–35 years at the time of loan application

Application Process

Most MBBS loan applications are now digital, making the process fast and hassle-free.

Step 1: Online Application

- Fill personal details, college name, course, and co-applicant details.

Step 2: Document Submission

- Admission proof, NEET score, fee structure

- ID & address proof of student and co-applicant

- Income proof of co-applicant

Step 3: Loan Sanction & Disbursal

- Verification by bank or NBFC

- Loan approval usually within 2–10 days

- Funds directly transferred to college

Platforms like Propelld provide instant eligibility checks and compare multiple lenders for the best terms.

Benefits of MBBS Education Loans

- Financial Accessibility: Covers tuition, hostel, and other educational expenses

- Flexible Repayment: Moratorium period and long tenure make EMIs manageable

- Unsecured Option: Up to ₹30 lakh without collateral

- Tax Benefits: Section 80E allows deduction on interest paid

- Online Convenience: Digital application and faster approval

Tips to Manage MBBS Loan Efficiently

- Plan Ahead: Apply as soon as you get admission to avoid last-minute stress

- Choose the Right Co-Applicant: Stable income and good credit reduce interest rate

- Compare Lenders: Check interest rates, processing fees, and repayment flexibility

- Use Online Platforms: Propelld and GyanDhan streamline application and comparison

- Budget Post-MBBS Income: Plan EMIs according to expected salary after internship

Popular Lenders for MBBS Education Loans

Banks Offering MBBS Loans

| Bank | Loan Amount | Interest Rate | Collateral Requirement |

| State Bank of India | ₹50L | 8.5–12% | Collateral above ₹7.5L |

| HDFC Bank | ₹45L | 9–11% | Property/fixed deposit |

| ICICI Bank | ₹50L | 9–12% | Collateral for high amounts |

| Axis Bank | ₹40L | 9–11% | Secured for large loans |

NBFC & Online Platforms

- Propelld: Instant eligibility, digital processing, collateral-free up to ₹30 lakh

- GyanDhan: Loan comparison, expert guidance, fast disbursal

Using online platforms helps students save time and select the best lender for their MBBS loan needs.

Real-Life Example with Calculation

Scenario:

- MBBS fee: ₹35,00,000

- Loan taken: ₹30,00,000 (unsecured) + ₹5,00,000 (secured with collateral)

- Interest rate: 9% per annum

- Moratorium: 6.5 years

- Repayment tenure: 10 years

Interest During Moratorium (Interest Capitalized):

Total loan after moratorium: ₹47,55,000

Monthly EMI for 10 years:

EMI≈₹62,000/month

This shows why planning repayment based on future income is essential.

Conclusion

An education loan for MBBS in private colleges is a valuable financial tool for students aspiring to become doctors. By understanding loan amounts, interest rates, repayment options, eligibility, and collateral requirements, students can make informed decisions and manage their finances efficiently. Platforms like Propelld and GyanDhan simplify the process by comparing lenders, calculating EMIs, and offering fast digital approvals.

Planning your loan carefully, selecting the right lender, and budgeting for EMIs after graduation ensures that your MBBS journey is smooth and stress-free. With proper guidance and smart financial planning, students can pursue their dream of becoming a doctor without worrying about high upfront costs.