Buying a home is one of the biggest financial decisions in life, and your mortgage rate plays a huge role in how much you finally pay. When people search for updates on home loans, one phrase keeps coming up everywhere — current fixed mortgage rates. Understanding these rates is extremely important if you want an affordable loan and manageable monthly payments.

This blog explains everything about current fixed mortgage rates in very simple language. You will learn what fixed rates are, why they matter, how they change, what affects your personal rate, and how you can calculate your monthly instalments with easy examples. By the end, you will feel confident enough to compare rates, make better choices, and plan your home purchase or refinance smartly.

What Are Current Fixed Mortgage Rates?

A fixed mortgage rate means the interest rate stays the same for the entire life of your loan. For example, if you take a 30-year fixed mortgage at 6%, that 6% stays the same for 30 years. It does not increase or decrease with market changes.

This gives homeowners stability, predictable payments, and peace of mind because your monthly instalment won’t suddenly rise.

The word “current” means the rate available in the market today. These rates change regularly because they depend on economic conditions, demand for mortgages, financial markets, and even global events.

Why Fixed Mortgage Rates Matter for You

Fixed mortgage rates are important because:

- They decide your monthly payment

- They decide how much total interest you will pay

- They help you plan your long-term finances

- They protect you from future rate increases

Even a small difference in the rate—like 6.0% vs 6.5%—can mean paying thousands of dollars more over time.

Types of Fixed Mortgage Rates

The two most common types are:

a) 30-Year Fixed Mortgage

- Most popular option

- Lower monthly payment

- Higher total interest

b) 15-Year Fixed Mortgage

- Higher monthly payment

- Loan finishes faster

- Much lower total interest paid

Both have their pros and cons. Buyers who want smaller monthly payments choose 30-year loans. People who want to finish the loan quickly choose 15-year loans.

Current Fixed Mortgage Rates

As of early, the market average fixed mortgage rates are around:

- 30-Year Fixed Rate: Approx. 6.19%

- 15-Year Fixed Rate: Approx. 5.44%

Remember, these are market averages, not the exact rates every bank will offer. Your own rate can be higher or lower depending on your financial profile.

How Fixed Mortgage Rates Change

Fixed mortgage rates change based on several factors:

a) Inflation

When inflation rises, interest rates usually rise too. This protects lenders from losing money.

b) Economic Conditions

If the economy is strong, rates may go up. If the economy slows down, rates often drop.

c) Bond Market

Mortgage rates are closely related to long-term government bond yields. When bond yields rise, mortgage rates usually rise.

d) Borrower Profile

Your rate depends on:

- Credit score

- Down payment

- Loan amount

- Debt-to-income ratio

- Type of property

- Employment stability

This is why two people applying on the same day at the same bank may get different rates.

Example: How Borrower Profile Affects Your Rate

Imagine two borrowers applying for the same loan amount of $300,000.

Borrower A

- Credit score: 780

- Down payment: 20%

- Debt-to-Income Ratio: 32%

Possible rate: 5.9% (lower risk to lender)

Borrower B

- Credit score: 640

- Down payment: 5%

- Debt-to-Income Ratio: 49%

Possible rate: 7.3% (higher risk to lender)

Even though the market average may be around 6.2%, Borrower A gets lower rates, and Borrower B gets higher rates.

This shows how personal financial health directly affects your final mortgage rate.

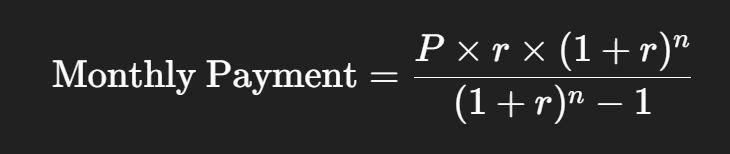

How to Calculate Your Monthly Mortgage Payment

Many buyers get confused about how monthly mortgage payments are calculated. The good news is the basic formula is simple.

Monthly Payment Formula (simplified):

Where:

- P = Loan amount

- r = Monthly interest rate (annual rate ÷ 12)

- n = Total number of payments (years × 12)

Let’s use an easy example.

Example Calculation: 30-Year Fixed Mortgage

Loan amount: $300,000

Annual interest rate: 6%

Loan term: 30 years (360 months)

Step 1: Convert annual rate to monthly rate

6% ÷ 12 = 0.5% per month

0.5% = 0.005

Step 2: Total number of payments

30 × 12 = 360

Step 3: Put values into formula

Monthly Payment≈$1,798

So, for a $300,000 loan at 6% interest over 30 years, the monthly payment is around $1,798.

Example Calculation: 15-Year Fixed Mortgage

Loan amount: $300,000

Annual interest rate: 5.5%

Loan term: 15 years (180 months)

Monthly rate = 0.055 ÷ 12 = 0.00458

Number of payments = 180

Using the formula:

Monthly Payment≈$2,451

So the monthly payment is higher, but the loan finishes much earlier.

Important Comparison (30-Year vs 15-Year)

| Feature | 30-Year Loan | 15-Year Loan |

| Monthly Payment | Lower | Higher |

| Total Interest Paid | Higher | Much Lower |

| Loan Finishes | Slow | Fast |

| Best For | Buyers wanting lower monthly cost | People who want to save interest |

Total Interest Difference Example

Let’s compare total interest paid on a $300,000 loan:

30-Year at 6%

Monthly: $1,798

Total paid over 30 years: $1,798 × 360 = $647,280

Interest paid: $647,280 − $300,000 = $347,280

15-Year at 5.5%

Monthly: $2,451

Total paid over 15 years: $2,451 × 180 = $441,180

Interest paid: $441,180 − $300,000 = $141,180

Interest Saved

$347,280 − $141,180 = $206,100 saved by choosing a 15-year loan.

This shows how much interest cost depends on your rate and loan term.

How to Get the Lowest Possible Fixed Mortgage Rate

a) Improve Your Credit Score

A score above 740 usually gets the best rates.

b) Increase Your Down Payment

20% down often gets you a better rate and avoids extra costs like mortgage insurance.

c) Reduce Debt Before Applying

Lower DTI = Better rate

d) Compare Multiple Lenders

Don’t accept the first rate you see. Even a 0.3% difference can save you thousands.

Example of Savings:

Loan amount: $350,000

Rate difference: 6.2% vs 5.9%

Difference in payment ≈ $70–$90 per month

Savings over 30 years can reach $25,000+

e) Choose a Shorter Loan if Possible

15-year loans usually come with lower interest rates.

Should You Lock Your Rate?

When you apply for a mortgage, lenders offer something called rate lock — a guarantee that your rate will not increase for a set time (usually 30–60 days).

Locking is smart when:

- Rates are rising

- You have found the right property

- You want payment certainty

Waiting can be risky if the market is unstable.

Should You Refinance Now?

Refinancing means replacing your old loan with a new one at a lower rate.

You should consider refinancing if:

- Your current rate is 1% or higher than today’s rates

- Your credit score has improved

- You want lower monthly payments

- You want to switch from a variable rate to a fixed rate

- You want a shorter loan term

Example: Refinance Savings

Old rate: 7.5%

New rate: 6.0%

Loan amount: $280,000

Monthly payment at 7.5% ≈ $1,958

Monthly payment at 6.0% ≈ $1,679

Monthly savings = $279

Yearly savings = $3,348

10-year savings = $33,480

This shows how refinancing at a lower fixed rate can save a huge amount of money over time.

Tips for Homebuyers

- Track rates weekly

- Improve credit before applying

- Avoid taking other loans just before applying

- Keep financial documents ready

- Save for a bigger down payment

- Compare at least 3–5 lenders

- Understand closing costs

- Always check if the rate includes discount points

The more prepared you are, the better your chances of getting a low fixed mortgage rate.

Final Thoughts

Current fixed mortgage rates play a major role in deciding how affordable your home becomes. While the average market rate is around 6.19% for 30-year loans and 5.44% for 15-year loans, your personal rate will depend on your financial profile, credit score, down payment, and lender choice.

Understanding how rates work, how to calculate monthly payments, and how to compare lenders gives you the power to make smarter financial decisions. Whether you’re buying a new home or refinancing, taking time to research current fixed mortgage rates can save you thousands of dollars over the life of your loan.

With the right knowledge and preparation, you can secure a rate that keeps your home affordable and your financial future strong.