Education loans are a great way to finance your higher studies without putting too much burden on your family. But before taking a loan, it is very important to know how much EMI (Equated Monthly Installment) you will have to pay every month after completing your studies.

In this blog, we will explain how is EMI calculated on an education loan with the help of a simple formula, examples, and tips.

Also Read: Can I Get an Education Loan Without Income Proof?

💡 What is EMI?

EMI stands for Equated Monthly Installment. It is the fixed amount that a borrower has to pay every month to the bank or financial institution to repay the loan. The EMI includes:

- Principal (the actual loan amount)

- Interest (cost of borrowing the money)

So, every EMI payment reduces your loan amount and pays some interest on it.

📐 How is EMI Calculated on an Education Loan?

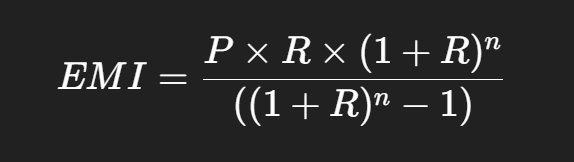

The EMI is calculated using a standard mathematical formula:

Where:

- P = Principal Loan Amount (₹)

- R = Monthly Interest Rate (Annual Rate ÷ 12 ÷ 100)

- n = Loan Tenure (in months)

🔢 Example: EMI Calculation for Education Loan

Let’s assume:

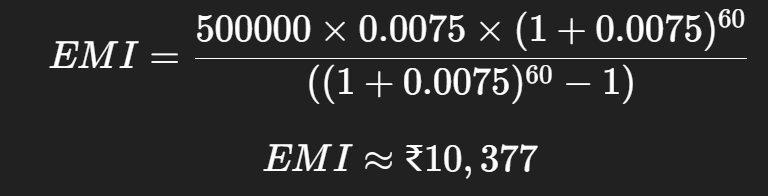

- Loan Amount (P) = ₹5,00,000

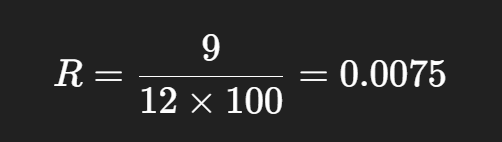

- Interest Rate = 9% per year

- Tenure = 5 years (60 months)

Step 1: Convert interest rate to monthly rate

Step 2: Use the EMI formula

So, your monthly EMI will be approximately ₹10,377 for 5 years.

📊 EMI Calculation Table for Different Loan Amounts

| Loan Amount (₹) | Interest Rate | Tenure (Years) | Approximate EMI (₹) |

| 2,00,000 | 9% | 5 | 4,150 |

| 4,00,000 | 9% | 5 | 8,300 |

| 6,00,000 | 9% | 5 | 12,450 |

| 8,00,000 | 9% | 5 | 16,600 |

| 10,00,000 | 9% | 5 | 20,750 |

Note: These are approximate values and may vary slightly depending on exact interest rates or bank rules.

📆 When Do You Start Paying EMI on an Education Loan?

Most banks provide a moratorium period during which you don’t have to pay EMI. This includes:

- Duration of the course +

- 6 to 12 months grace period after course completion

You start paying EMIs after this period ends, also known as the repayment period.

🧾 What Affects Your EMI?

Here are the main factors that affect how much EMI you pay:

- Loan Amount (P): Higher the loan, higher the EMI.

- Interest Rate (R): Higher rate = more EMI.

- Loan Tenure (n): Longer tenure = smaller EMI, but you pay more total interest.

🧮 Use Online EMI Calculators

You don’t need to calculate EMI manually. Banks provide online EMI calculators like:

- BankBazaar Education Loan EMI Calculator

- Axis Bank Education Loan EMI Calculator

- Union Bank EMI Calculator

Just enter:

- Loan Amount

- Interest Rate

- Loan Tenure

And it shows the exact EMI and repayment schedule.

🧠 Tips to Manage Your Education Loan EMI Smartly

- Start saving during your study period to reduce burden later.

- Try to pay more than the EMI to reduce your loan faster.

- Opt for lower interest rate banks or use government schemes.

- Avoid delaying EMI payments to keep your credit score good.

📌 Conclusion

Understanding how EMI is calculated on an education loan helps you plan your future better. Whether you are studying in India or abroad, knowing your monthly repayment amount ensures there are no surprises later.

Always compare different bank offers, check EMI using online calculators, and choose a loan that fits your budget. Remember, education is an investment—and smart planning makes repayment stress-free.